Poster Session 2 · Wednesday, December 3, 2025 4:30 PM → 7:30 PM

#2710 Spotlight

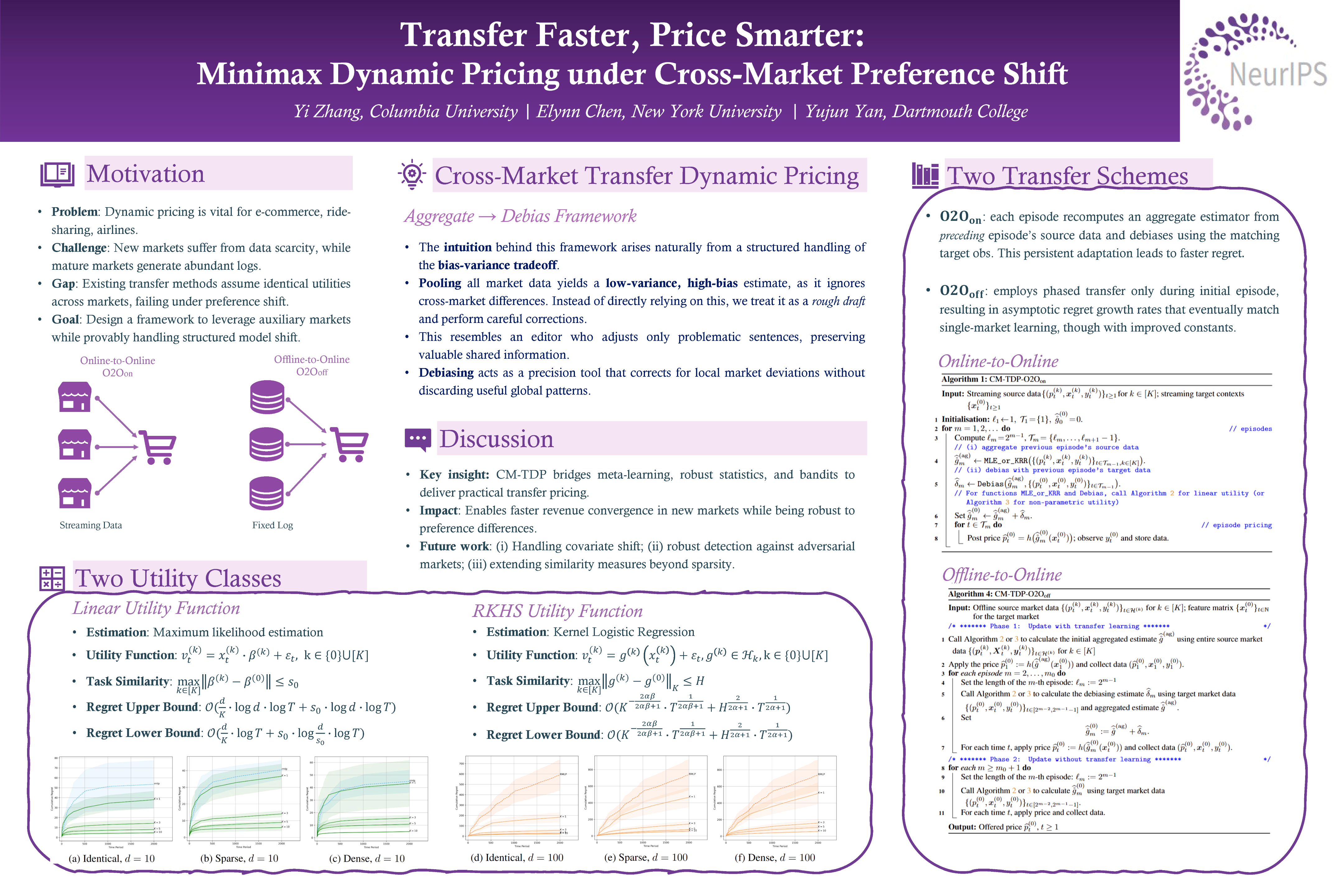

Transfer Faster, Price Smarter: Minimax Dynamic Pricing under Cross-Market Preference Shift

Abstract

We study contextual dynamic pricing when a target market can leverage auxiliary markets—offline logs or concurrent streams—whose mean utilities differ by a structured preference shift. We propose Cross-Market Transfer Dynamic Pricing (CM-TDP), the first algorithm that provably handles such model-shift transfer and delivers minimax-optimal regret for both linear and non-parametric utility models.

For linear utilities of dimension , where the difference between source- and target-task coefficients is -sparse, CM-TDP attains regret . For nonlinear demand residing in a reproducing kernel Hilbert space with effective dimension , complexity and task-similarity parameter , the regret becomes , matching information-theoretic lower bounds up to logarithmic factors. The RKHS bound is the first of its kind for transfer pricing and is of independent interest.

Extensive simulations show up to 38% higher cumulative revenue and faster convergence relative to single-market pricing baselines. By bridging transfer learning, robust aggregation, and revenue optimization, CM-TDP moves toward pricing systems that transfer faster, price smarter.