Poster Session 6 · Friday, December 5, 2025 4:30 PM → 7:30 PM

#3102

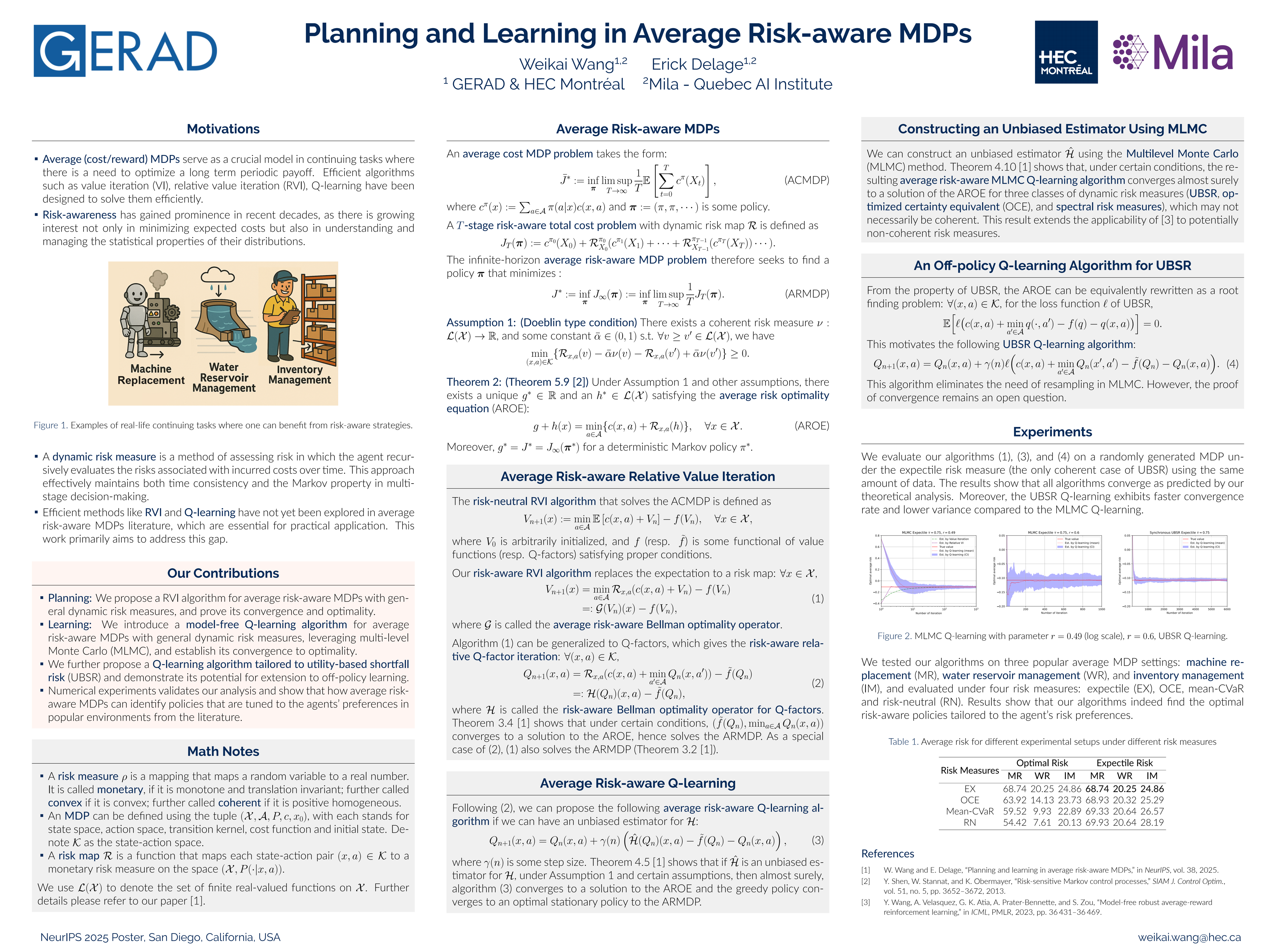

Planning and Learning in Average Risk-aware MDPs

Abstract

For continuing tasks, average cost Markov decision processes have well-documented value and can be solved using efficient algorithms. However, it explicitly assumes that the agent is risk-neutral.

In this work, we extend risk-neutral algorithms to accommodate the more general class of dynamic risk measures. Specifically, we propose a relative value iteration (RVI) algorithm for planning and design two model-free Q-learning algorithms, namely a generic algorithm based on the multi-level Monte Carlo (MLMC) method, and an off-policy algorithm dedicated to utility-based shortfall risk measures.

Both the RVI and MLMC-based Q-learning algorithms are proven to converge to optimality. Numerical experiments validate our analysis, confirm empirically the convergence of the off-policy algorithm, and demonstrate that our approach enables the identification of policies that are finely tuned to the intricate risk-awareness of the agent that they serve.