Poster Session 6 · Friday, December 5, 2025 4:30 PM → 7:30 PM

#2805

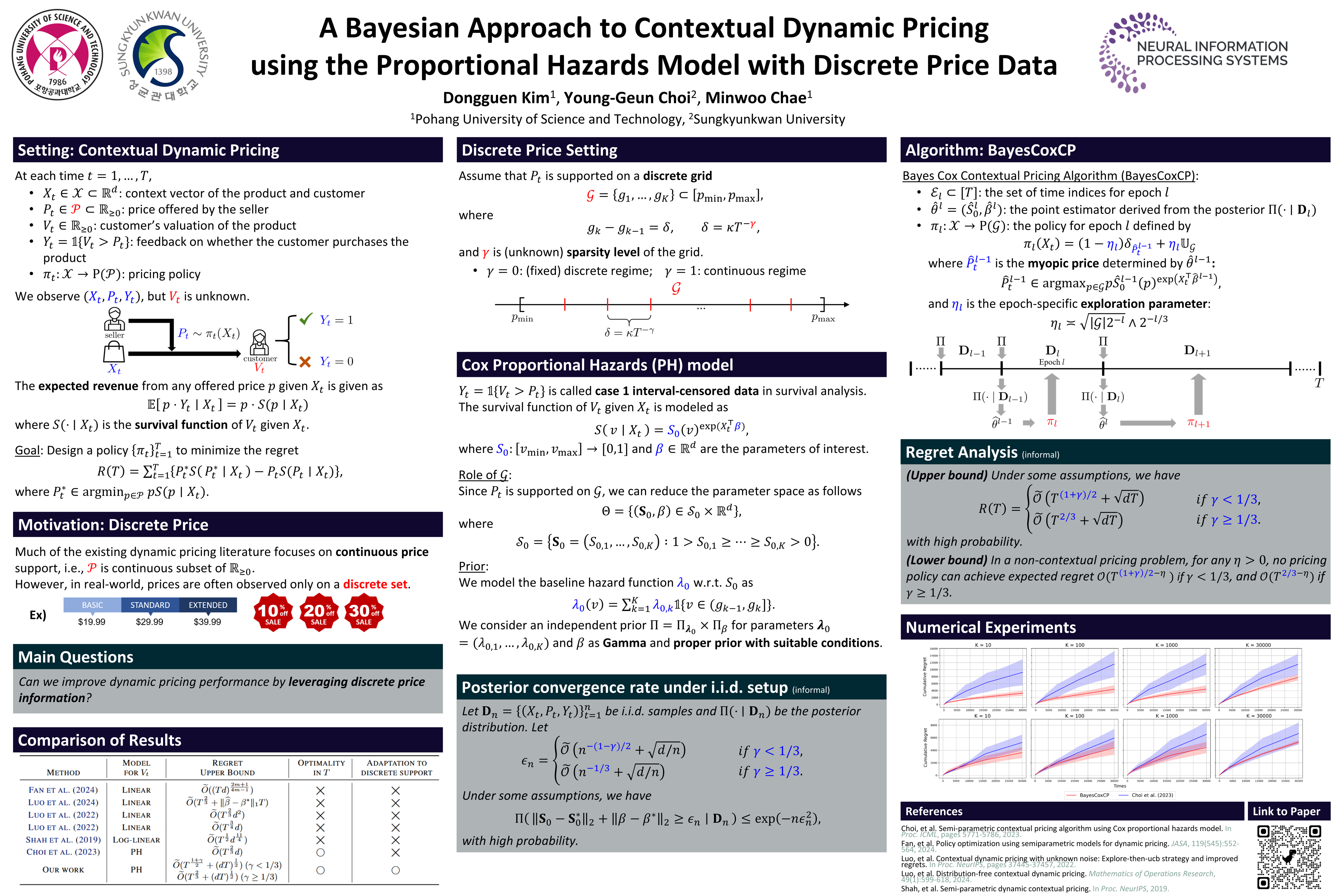

A Bayesian Approach to Contextual Dynamic Pricing using the Proportional Hazards Model with Discrete Price Data

Abstract

Dynamic pricing algorithms typically assume continuous price variables, which may not reflect real-world scenarios where prices are often discrete. This paper demonstrates that leveraging discrete price information within a semi-parametric model can substantially improve performance, depending on the size of the support set of the price variable relative to the time horizon.

Specifically, we propose a novel semi-parametric contextual dynamic pricing algorithm, namely BayesCoxCP, based on a Bayesian approach to the Cox proportional hazards model.

Our theoretical analysis establishes high-probability regret bounds that adapt to the sparsity level , proving that our algorithm achieves a regret upper bound of for and for , where represents the sparsity of the price grid relative to the time horizon .

Through numerical experiments, we demonstrate that our proposed algorithm significantly outperforms an existing method, particularly in scenarios with sparse discrete price points.